You Are Enough

I do things differently. I'm not in a box, and I'm not for everyone. I like to talk about behaviours, psychology, emotions, trauma, spirituality and how our beliefs are built, along with teaching my skill set when it comes to finances. I tend to talk about things that are considered "taboo" and most may shy away from on a public platform. I like the idea of putting all this together and pushing the limits and the narratives we live by.

Our financial world needs a change, one that is more open, accepting and compassionate of one's situation. One that educates instead of sells, one that puts client relationship, trust and integrity at the top. We need more compassionate, judgement free zones where we have permission to take off our masks we hide behind.

I support women; single working moms, corporate mom's, divorcee's, widows and provide financial empowerment education. As a Single Divorced Working Mother (and yes, that deserves a title with all the capitals!) I know you well. I know the challenges of being a single mom, I know the emotional and financial toll divorce takes, I know the shame and guilt that comes with being a single mom, while navagating the pressure of wanting to provide the life we always dreamed of for children. These emotions run deep, and in finance we need to be going deeper. We need to be changing how we look, feel and manage money in order to make any lasting change.

Did you know that we all have a unique money story, just as we each have our own unique personal journey?

The way we were raised, the narrative we were taught, the discussions or arguments witnessed in childhood all carry forward to adulthood in ways you may not even be aware of.

In my discussions with many single working moms, their biggest worry was not giving or providing enough for her children. One Mom in particular was the amount of downsizing she had to do after her divorce.

She went from a large grand home, to a 2 bedroom apartment with 2 kids and she held so much guilt and shame for this, she continued to beat up on herself as she didn't feel like she was enough of a mom because of this, and if she could just get back what she had, it would be different.

This story also hits close to home, it was interesting as she spoke these words, she was describing my life 10 years ago freshly out of a marriage, walking away from everything I had owned including my house and into a 2 bedroom condo with 2 children on the "bad side of town". I felt her words deeply, knowing exactly the shame, sadness and pain she was feeling. As I probed her for the root of the pain, I asked what her childhood conditions were like, there, in that moment the lightbulb turned on. "Oh my goodness, we lived in low income housing," she said. "I was always so embarrassed, I always told myself that I would do better with my life. I never wanted people to see where I lived, I would be asked to be dropped off blocks away from my house."

These experiences shape who we are. Much like her as a kid I was raised by a single mom who worked three jobs, I told myself at a young age I would never let my kids know what never having enough felt like. And, in my darkest days, during my divorce while navigating being a single Mom, I shared the same feelings she was experiencing. When my 5 year old definition, my reality, my feeling of "didn't have enough" was now true.

But, what if at that time I knew more, what if I knew to question my beliefs? What if I knew this was a belief I currated from when I was a little girl experiencing lack, and it no longer has to be true? Can we challenge that thought and do the work to install a new belief?

This is why I’m here, to teach and bring awareness. AND, this is where YOUR work is if you find yourself resonating!

If you don't start to ask questions around why you operate and think the way you do, you will forever be living in your conditioned state of being. Our emotions run our money, our money story can get in the way of true wealth and happiness. Financial management and wealth creation are a piece of the puzzle. In order to live a truly fulfilled WEALTHY life we need to dig deeper into our stories, and investigate with no longer holds value, and then, how can we transform it into something that does provide value?

What’s Your Definition of Wealth?

Next January I’ll have been in the finance industry for two decades.

Two decades.

I started young, let’s keep that in mind, but still. Twenty years of sitting across from people at some of the most vulnerable and pivotal moments of their financial lives. Twenty years of watching what money does to people. And what people do to money.

And here’s what all of that time has taught me more than anything else:

Money is only one piece of the wealth pie.

It’s an important piece. A real one. I’m not going to sit here and tell you money doesn’t matter — it does. It’s a tool. It creates options. It buys freedom and safety and experiences and opportunity. I use it to build a life for my girls and I take that seriously.

But I have sat across from people with substantial wealth who were deeply, quietly miserable. And I have sat across from people with far less who radiated something I can only describe as fullness.

So when I think about what wealth actually means to me — it’s this:

It’s feeling fulfilled from the inside out. It’s contentment that doesn’t depend on a number. It’s catching a fleeting moment and actually being present in it instead of rushing past it. It’s living so aligned with who you are that your energy becomes magnetic, and the right people, opportunities and blessings find their way to you.

It’s riding the edges of your comfort zone because you know that’s where you grow.

It’s the small moments you almost took for granted.

Wealthy isn’t a balance. It’s a feeling. And it starts from within.

So I’ll ask you what I ask myself:

What does wealth mean to you?

Has your self worth been tied to your career, and security to money?

A question not typically asked or understood, because of how vulnerable it is to even consider.

I wouldn’t have questioned it myself until I started digging deep and realizing how much of mine was.

Here’s what I learned about wealth and career when I decided to step away from my professional titles and the identity of being a “successful corporate woman.”

I’ve been in Finance for over two decades. I grew up in the corporate world and very much adopted the mentality of excelling, performing, pushing myself and exceeding. I created this linear illusion of success that validated my power and worth. As long as I was climbing the corporate ladder I felt worthy. As long as I had money in my bank with some zeros behind it I felt like I was somebody. As long as I had initials behind my name and a position of power I felt strong and confident.

I tied my worth entirely to my career. It became my identity. The money in my accounts was a form of security, albeit a false one, because no matter how much I had I never felt secure. I was always operating from lack. I had inadvertently built my worth outside of myself, and it was conditional on how much I achieved.

It took intentional healing and slowing down to confront that truth. It wasn’t pretty. I chose to deconstruct who I had built myself to be. I let go of titles and other people’s definitions of who I was, along with beliefs and behaviours that were no longer serving me.

This is part of being human. When we start asking the hard questions we begin to heal. We stop making excuses and start cultivating our own inner richness, building a life from the inside out, not outside in. We stop trying to fit someone else’s definition of success and give ourselves permission to evolve into our next version of self.

Here’s what I know after doing this work on myself and sitting with hundreds of women doing the same: real wealth was never in the account balance. It was never in the title. It was never in the initials after your name. It was always in the relationship you have with yourself, your values, your peace, your sense of enough.

That’s the wealth that doesn’t disappear when the market drops. That’s the wealth nobody can take from you..

____________________________________

Do you want to feel more empowered with your finances and learn to live an abundant life aligned to your inner richness — not reliant on your bank account? If this resonated, I’d love to connect.

We all need teammates. I’d like to be yours.

Don’t walk, RUN! The market is on sale!

The S&P 500 has lost 15% of its value since the beginning of this year.

Market crash/correction sounds scary, when in reality, history has shown its just a blip on the radar long term;

I’m not discounting the fear, the fear is real and I’m here to say you are allowed to feel that, but do NOT let the media sway you, do not let friends talk you into changing ANYTHING! Do not talk to your neighbour and take their tips and make a move you will later regret. Do not move! Avoid emotional knee jerk reactions and filter out the noise to avoid mistakes. (See my earlier post around emotional investing)

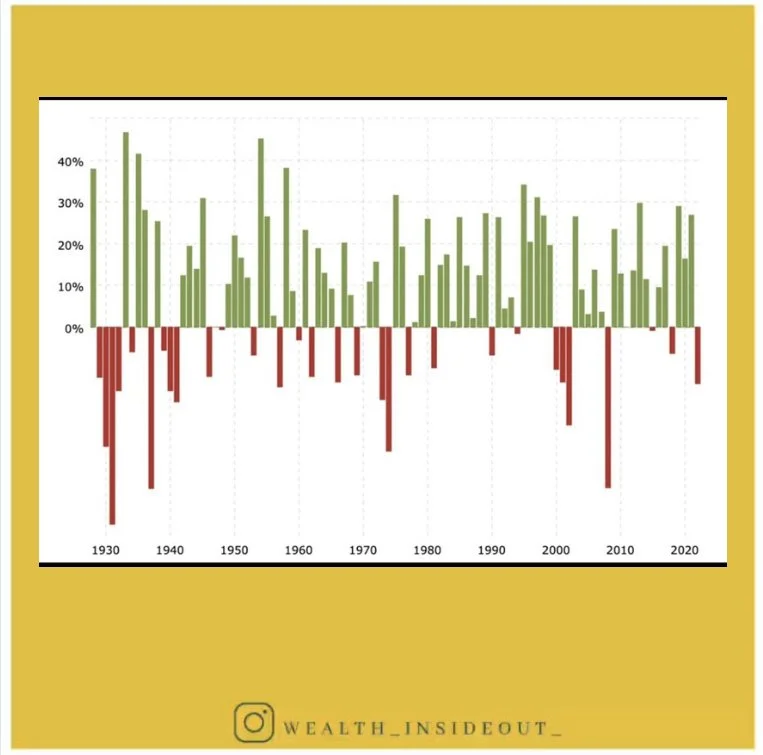

Market corrections are a normal part of investing. Since 1928, we've had 26 bear markets (decline) in the S&P 500, and 27 bull markets (incline). Gains during bull markets far outweigh the losses of bear markets.

Remember, we are playing the long game, (your money SHOULD NOT be in the market if it’s short term - it’s too risky!) and when investing for the long term this now provides you an opportunity to buy more shares at cheaper price to realize gains later.

Statistically, stocks lose an average of 36% in a bear market and gain an average of 114% in a bull market.

I read a great analogy today;

“When the shoes you love go on sale, we probably buy another pair in a different colour! We don’t try and sell our loved shoes at a discount”

Or how about this one;

“when you were dating in high school, and your partner broke up with you, At the time it’s devastating. 10 years later it’s pretty insignificant overall”

Bear markets can be an opportunity instead of panic! An opportunity to buy at a cheaper price.

If you are anxious and unsure this is the time having an advisor will pay dividends, reach out to them, or they should be reaching out to you to check in and smooth concerns. I went through the crash in 2008 with my clients, some unfortunately fear got the best of them, no matter what I had to say and they chose to cash in never recouping the loss, while the majority has a distant memory stayed invested for the long haul and reaped the rewards especially in 2013!

Albeit it was a bumpy, emotional and tremulous time for all involved - as an advisor we have our finger on the pulse, let us do what we do best.

You can refer to this graph for the bull (green) and bear (red) markets to show the history of the market and after a bear, always follows with a bull market to capitalize on.

Avoid Emotional Investing

People naturally tend to become emotionally invested in their own portfolios. They become overly greedy when markets are up and overly fearful when markets are down. The reasons for these attitudes are well documented by behavioural economics.

Having an Advisor keeps your emotions away from the investment process, amid all the volatility and unpredictability that markets show, the ultimate value of a planner is to keep you focused and in your seat. Focused more on your long term goals than the short term volatility of your portfolio. A really great article I read said, "A good Advisor will protect you, from you. No, your advisor can't stop you from feeling whatever emotions you're feeling, just like a guardrail can't stop every car from going into the ditch. In those moments where you want to push the eject button because you're scared, the advisor's job is to remind you of the plan you created and what you're working towards: "a fulfilling and successful retirement."

Good advisors help you navigate your emotions and coach you through choppy storms.

Isn't it also nice to have a partner for your journey to financial wholeness? Having someone in your corner who's as invested in your success as you are? I'm talking about an advisor who thoroughly knows you, your spouse, your kids, your dream job, your hopes and aspirations for your future. Someone who cares about you, knowing that your advisor truly has your best interest at heart is psychologically impactful. Just as people hire personal trainers or business coach's the advisor sets your up for success and roots for you every step along the way. If you don't have a connection with your advisor, I'd suggest you keep looking until you find one because they will make a world of difference.

Behavioural Study and Loss Aversion in Investing

It’s been a bumpy ride, I won’t deny that. Markets are volatile, the world is volatile.

Stay in your seat!

At this point in time I’d like to turn your attention to behavioural biases you may be consuming, and the instinctive human nature to loss aversion.

Are the messages you receive all doom and gloom? Are they from credible sources? How much attention are you giving to the negative and catastrophizing? Are you now only focused on short term vs. long term planning?

Again, this is not the time to do anything except lean on your advisor, or credible sources who understand how the market moves. Please see my blog post “Emotional Investing”

I met with a woman yesterday who wanted a second opinion on her portfolio because she “lost” quite a bit of money. Scrambling, experiencing many REAL and EXPECTED reactions to her financial statements, she wanted to pull all of it out to “stop the bleeding.”

Here’s also where loss aversion comes into play. Loss aversion in behavioral economics refers to a phenomenon where a real or potential loss is perceived by individuals as psychologically or emotionally more severe than an equivalent gain. For instance, the pain of losing $100 is often far greater than the joy gained in finding the same amount.

Sociologists point to the fact that we are socially conditioned to fear losing, in everything from monetary losses but also in competitive activities like sports and games to being rejected by a date. Or, fear that keeps you stuck in the same spot, I learned a lot about this in my Psychology and Neuroplasticity courses and its fascinating!

Investors can avoid psychological traps by adopting a strategic asset allocation strategy with their advisor, think rationally, and not let emotion get the better of them.

I want to remind you, that you do not lose until you cash it in! And, moving to a lower risk investment may slow the decline, but remember you will miss the incline! And, the incline WILL come. If you make a move now, you’ve lost. If you lower your risk it may look better in the short term, but not in the long term if we could extrapolate out.

Below is a graph of the bull (green) and bear (red) markets. Being an advisor in 2008 was treacherous, it WAS NOT a fun time. People did pull out at the bottom, against professional advice, please note the growth that proceeded the downturn.

Keep you bum in the seat!